今回は、前回紹介したパフォーマンス要因分析手法の一つである、ブリンソン型の要因分析を実際にPythonで実装してみたいと思います。

設定とデータ取得

今回は、TOPIX Mid400の銘柄の等ウェイトをポートフォリオに設定し、ベンチマークをTOPIXとして分析を行ってみたいと思います。

まずは、必要なデータとして、TOPIXのウェイトデータと、ポートフォリオウェイト、ベンチマークウェイトを作成します。

import requests

import pandas as pd

import yfinance as yf

#TOPIX銘柄コードの取得

# CSVファイルのURL

url = "https://www.jpx.co.jp/markets/indices/topix/tvdivq00000030ne-att/topixweight_j.csv"

# HTTPリクエストを送信してファイルをダウンロード

response = requests.get(url)

# ステータスコードが200(成功)の場合

if response.status_code == 200:

# ダウンロードしたCSVデータをファイルに保存

with open("topixweight_j.csv", "wb") as f:

f.write(response.content)

# ファイルをPandas DataFrameに読み込む

data_df = pd.read_csv("/content/topixweight_j.csv",encoding='shift-jis')

else:

print(f"Failed to download the file. Status code: {response.status_code}")

port_weight = data_df[data_df['ニューインデックス区分']=='TOPIX Mid400'][['コード']]

port_weight.columns = ['code']

port_weight['code'] = port_weight['code'].astype(int).astype(str) + '.T'

port_weight['weight'] = 1/len(port_weight)

bm_weight = data_df[['コード','TOPIXに占める個別銘柄のウエイト']].dropna()

bm_weight.columns = ['code','weight']

bm_weight['code'] = bm_weight['code'].astype(int).astype(str) + '.T'

bm_weight['weight'] = bm_weight['weight'].str.replace('%','').astype(float)/100

続いて、セクター情報を取得します。

sector_data = data_df[['コード','業種']].dropna()

sector_data.columns = ['code','sector']

sector_data['code'] = sector_data['code'].astype(int).astype(str) + '.T'

df_weight = pd.merge(port_weight, bm_weight, on='code',suffixes=['_port','_bm'],how='outer').fillna(0)

df_weight = pd.merge(df_weight, sector_data, on='code')

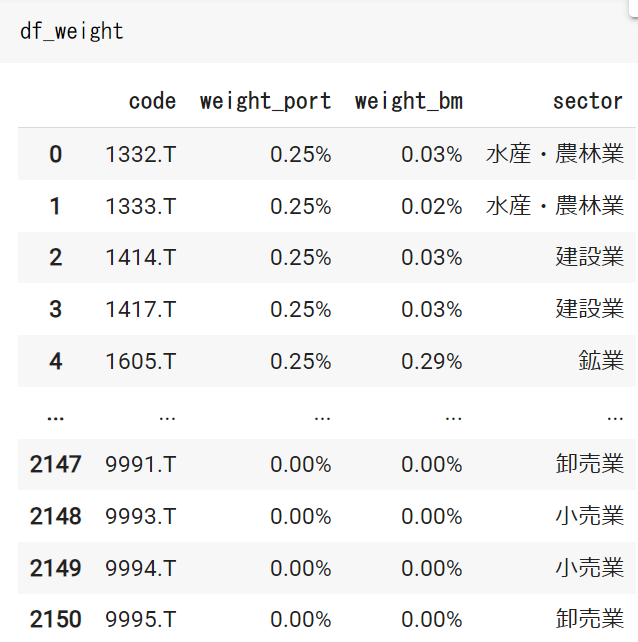

これらをまとめた情報であるdf_weightは次のようになります。

続いて、リターンデータをYahoo Financeから取得します。

from datetime import datetime, timedelta

today = datetime.now()

# 月初日を計算

first_day_of_month = today.replace(day=1)

date_s = first_day_of_month.strftime("%Y-%m-%d")

price = yf.download(list(df_weight['code']), start=date_s)

rtn = pd.DataFrame(price.iloc[-1,:]['Adj Close'] / price.iloc[0,:]['Adj Close'] - 1 ).reset_index()

rtn.columns = ['code','rtn']

データの準備が整いました。

ブリンソン型の要因分析

まずは取得したデータを整理し、ベンチマークリターンとポートフォリオリターンを作成します。

続いて、セクターごとのポートフォリオのリターンと、ベンチマークのリターンも計算しておきます。

df = pd.merge(df_weight, rtn, on=['code'])

def cal_weight(x, name='weight'):

return x[name]/x[name].sum()

weight_sector_bm = pd.DataFrame(df.set_index('code').groupby('sector').apply(cal_weight, name='weight_bm')).reset_index()

weight_sector_port = pd.DataFrame(df.set_index('code').groupby('sector').apply(cal_weight, name='weight_port')).reset_index()

df = pd.merge(df, weight_sector_bm.loc[:,['code','weight_bm']],on='code',suffixes=['','_sector'])

df = pd.merge(df, weight_sector_port.loc[:,['code','weight_port']],on='code',suffixes=['','_sector'])

df['rtn_bm'] = df['rtn'] * df['weight_bm_sector']

df['rtn_port'] = df['rtn'] * df['weight_port_sector']

df['weight_rtn_bm'] = df['weight_bm'] * df['rtn']

df['weight_rtn_port'] = df['weight_port'] * df['rtn']

df_sector = df[['weight_port','weight_bm','rtn_port', 'rtn_bm', 'sector','weight_rtn_bm','weight_rtn_port']].groupby('sector').sum()

アロケーション効果、セレクション効果、複合効果をそれぞれ計算します。

sector_effect = pd.DataFrame((df_sector['weight_port'] - df_sector['weight_bm']) * df_sector['rtn_bm'], columns=['アロケーション効果'])

selection_effect = pd.DataFrame((df_sector['rtn_port'] - df_sector['rtn_bm']) * df_sector['weight_bm'], columns=['銘柄選択効果'])

comb_effect = pd.DataFrame((df_sector['weight_port'] - df_sector['weight_bm']) * (df_sector['rtn_port'] - df_sector['rtn_bm']), columns=['複合効果'])

ベンチマークのリターン、ポートフォリオのリターンをそれぞれ計算し、結果をまとめます。

bm_rtn = (df['weight_bm'] * df['rtn']).sum()

port_rtn = (df['weight_port'] * df['rtn']).sum()

print(f'benchmark return : {bm_rtn:.2%}')

print(f'portfolio return : {port_rtn:.2%}')

result = pd.merge(sector_effect, selection_effect,right_index=True, left_index=True)

result = pd.merge(result, comb_effect, right_index=True, left_index=True)

result = pd.merge(df_sector['weight_rtn_bm'], result, right_index=True, left_index=True)

result = pd.merge(df_sector['weight_rtn_port'], result, right_index=True, left_index=True)

result.columns = ['ポートフォリオ','ベンチマーク','アロケーション効果','銘柄選択効果','複合効果']

result.loc['合計',['ポートフォリオ','ベンチマーク','アロケーション効果','銘柄選択効果','複合効果']] = result.sum()

実行すると次のような結果を得られます。

今回のコードはこちらのGoogle Colabで確認できます。